Is the market heading for a crash?

Short answer, inevitably at some point. Duh! The better questions are, When will this be? How bad will it be? Where will the epicentre of the crash be? And what sort of collateral damage can we expect?

I don’t have the answers to much of this. No one does. So let’s have a look at what we do know, as it may at least help us to decide whether it is wise / safe to invest in the equity market right now. And if not, what mitigating factors might be looked at to offset any crash, when or if it comes.

One of the first things to consider is, is the market in a bubble right now?

What seems reasonable to assert is that there are parts of the market that don’t appear to be supported by fundamentals - some of the AI-adjacent stocks for example. But there are also large parts that still are (most of the rest). The trailing P/E of the S&P 400 Midcap stocks is a little under 20, a bit higher than the ten year median of about 18.4, but not massively out of whack. Here at least, sanity still prevails.

In the information technology sector of the S&P 500, PEs are closer to 40, though even then, this may be justifiable depending on your view of how current investment will lead to earnings growth. So perhaps cause for caution, but maybe not yet panic. Would you pile into the sector? It may still be worth a dabble, but you’d want to ensure some less speculative elements to your portfolio if so.

Traditionally, most portfolio investors would do this with a slug of bonds. But right now, I’d be doing this carefully as well. I’m not 100% sure that the traditional negative relationship between equity prices and bonds will hold in the event of a crash. Currently, the correlation is not well defined. Where it goes to next will depend on the nature of any shocks. So for example, if we are still not out of the woods when it comes to inflation, and the next shock comes from this direction, then don’t expect your Treasury holdings to help you out.

And I raise this spectre not because necessarily there are any smoking guns in the economic data, though inflation remains sticky in some sectors and geographies, but because geopolitical risks that could deliver an unwelcome inflation shock remain highly plausible threats. For example, we still await the replacement of the highly respected (though not by President Trump) Chair of the Federal Reserve with - well, let’s be clear, a stooge, who will be expected to drive US short- term policy rates lower. And that is only likely to help unleash inflationary demons if done aggressively. Further attempts to undermine the independence of the Fed will also raise questions about the sanctity of the US Treasury market, and so while overseas bond markets are not without their problems, and there is likely to be considerable spillover, it might be worth looking at holding some other high investment grade government bonds instead, or for overseas investors, your local Treasury equivalent to get rid of currency risk as well.

It might also be worth considering shorter-term money-market instruments and shorter-maturity bonds as the yield curve is still fairly flat - you only get about 50bp from moving from the front end to the 10Y segment, and I’m not sure I want to take the duration risk of longer than that, even if the yield pick up is a bit more. So for the time being at least, front-end seems sensible as a principal protection hedge.

And in terms of currency, the two to watch (I think) will be the JPY and the USD. WIth 30Y JGB yields now heading up towards the 4% level, and 10Y JGB yields well over 2%, the rationale for holding USTs is looking less obvious. That, together with some rather fractious international tensions recently over events such as Greenland and NATO may make some investors less willing to just hang on to USTs as a default option. If that happens, then expect recent JPY weakness to reverse, and USD weakness to keep going - could be a good time to reconsider EUR, GBP, AUD etc..?

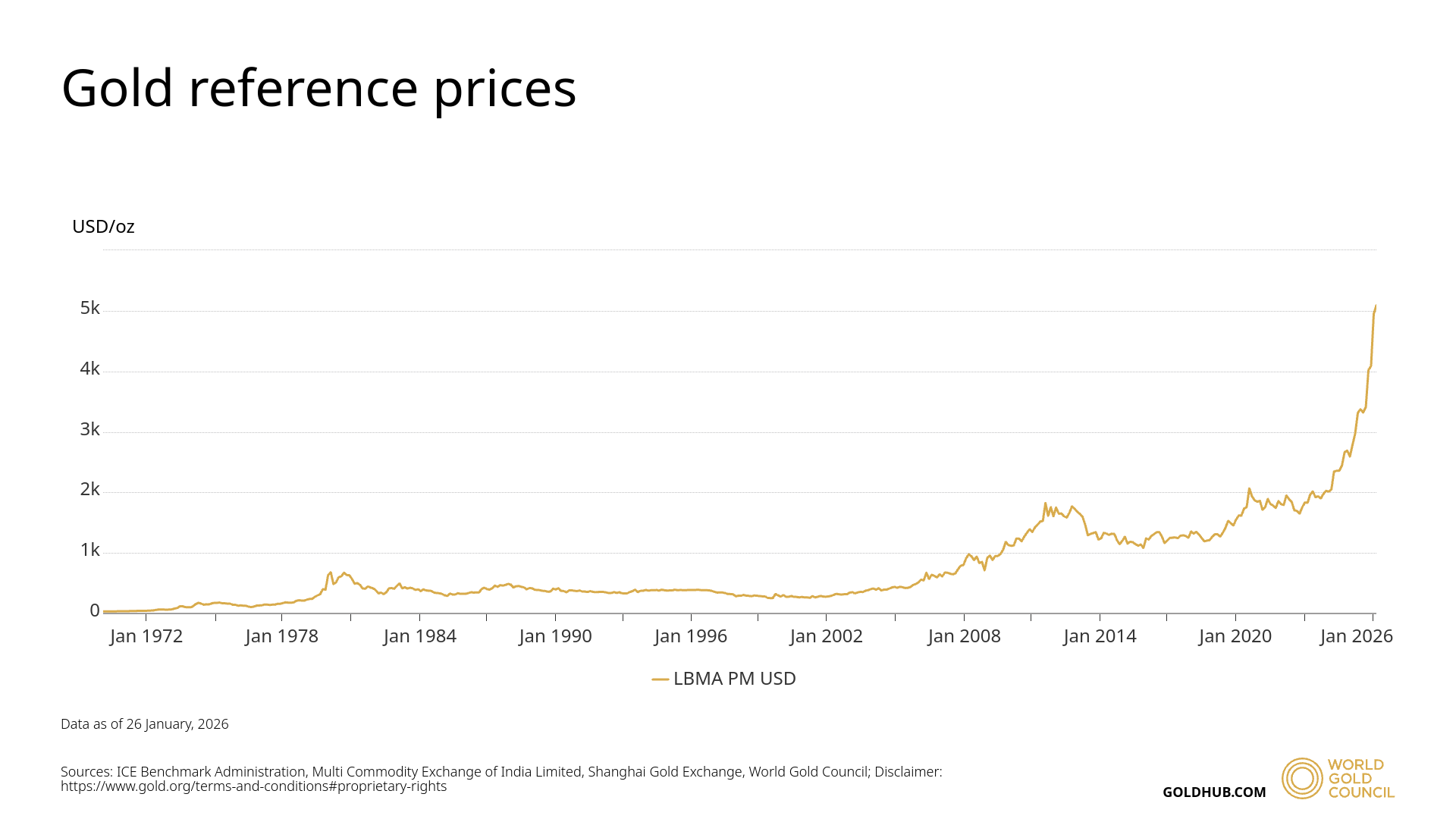

Traditionally, gold has been a nice haven in the even of inflation risk. But the recent price action is worth considering. As gold shot up through $5000/oz, it really did begin to resemble old bubble charts, like the Nikkei in the late 1980s or the US housing market in 2005/6. That point in the valuation of any asset where it starts to rise exponentially higher, based only on the greater fool theory of not wanting to miss out on a one way trade - never ends well! So should you sell out of gold? I have to admit to reducing my exposure recently after a very good run, though I still like it as an apocalypse insurance policy when Fiat currencies are fully undermined and electronic money wiped by cyberwars.

In all of this apocalyptic musing, it is worth considering the following though. Risk assets, including the equity market (I lump most corporate bonds into this too), tend to keep making gains long past the point when it looks like a good time to sell. Those turning points can really get drawn out for years past when you think they should turn. Aggressive central bank easing has in times past been a factor driving this. And with nothing on the fiscal side really to be expected from debt-ridden government coffers (Japan keeps trying, but does anyone really expect stimulus packages to do anything useful anymore?), central banks will likely keep the party going for longer if we experience an old-fashioned demand driven downturn. A supply / inflation shock would be a far harder problem for them to address while simultaneously keeping stocks afloat, and for that reason, I’d be watching the inflation indicators and signs of inappropriate easing from CBs as more urgent signals for a more defensive position.

One final warning - The FT’s Katie Martin opined at the beginning of the year that 2026 would not spell a crash for markets, having previously been quite bearish. Contrarian indicator? We will see….!